Stanford Woods Institute dropped their analysis showing California homeowners insurance premiums jumped 84% since late 2020. What that actually means at the job site is a crew chief in San Bernardino having to explain to a homeowner that their FAIR Plan coverage wouldn't touch the $18,000 replacement they needed. The homeowner had no idea their backup insurance only covered $12,000 max for roof damage.

This is happening across every California market right now. Not just fire zones — regular suburban neighborhoods from Sacramento to San Diego are seeing homeowners pushed into FAIR Plan or dealing with deductibles that went from $1,000 to $7,500 in three years.

For roofing contractors, this insurance squeeze creates an operational mess that most crews aren't prepared for. You're basically running a different business model when half your customers have restricted coverage or massive deductibles they can't afford upfront.

The coverage gap is breaking traditional roofing workflows

Most roofing operations built their processes around standard insurance claims — full replacement minus a reasonable deductible. That model assumed adjusters would approve legitimate damage, homeowners could handle their deductible, and supplemental claims would get processed for discovered damage.

That world doesn't exist in California anymore.

What's happening instead: homeowners with FAIR Plan coverage that caps roof damage at arbitrary limits, standard carriers requiring 2% deductibles on $800,000 homes (that's $16,000 out-of-pocket), adjusters denying wear-and-tear claims that would've passed two years ago, and supplemental approvals taking 45+ days instead of the usual 10-15.

A Fresno contractor showed me their receivables last month — $340,000 in unpaid work, mostly tied up in disputed claims or waiting on homeowner financing. Three years ago, their receivables never broke $80,000.

The operational strain shows up everywhere. Crews sitting idle waiting for approval on discovered damage. Sales reps spending hours explaining coverage limitations instead of closing deals. Office staff chasing three different insurance entities for a single job. Cash flow getting strangled by 60-90 day payment cycles.

Why standard documentation fails with restricted coverage

Most contractors are still documenting jobs like it's 2019. Take photos of obvious damage, write up a basic scope, submit to insurance, wait for approval. That approach gets you nowhere when coverage is thin and adjusters are looking for any reason to minimize payouts.

Keep every roofing job on track and on time.

Roofyly helps you manage, schedule, and communicate every roofing project with precision and ease.

- Centralized project planning

- Real-time crew notifications

- Integrated scheduling & client updates

No credit card required

The documentation bar has moved. Adjusters want proof that damage wasn't pre-existing. They want manufacturer documentation showing the damage exceeds normal wear. They need weather event correlation. They're asking for structural engineer reports on issues that used to get waved through.

A Riverside crew lost a $22,000 claim because their initial photos didn't capture the water intrusion pattern clearly enough. By the time they got back on the roof for better documentation, the adjuster claimed they couldn't prove the damage wasn't caused by their own tear-off process.

That same crew now runs a completely different protocol. Every job starts with a 360-degree video walkthrough before anyone touches anything. Minimum 40 photos during initial inspection — wide shots, close-ups, and measurement references for every damaged area. They document the weather history for the property going back 6 months. They pull manufacturer specs for the existing material to establish life expectancy baselines.

Overkill for standard insurance, maybe. But for FAIR Plan claims or high-deductible situations, this level of documentation is the difference between getting paid and eating a loss.

Building approval workflows around claim uncertainty

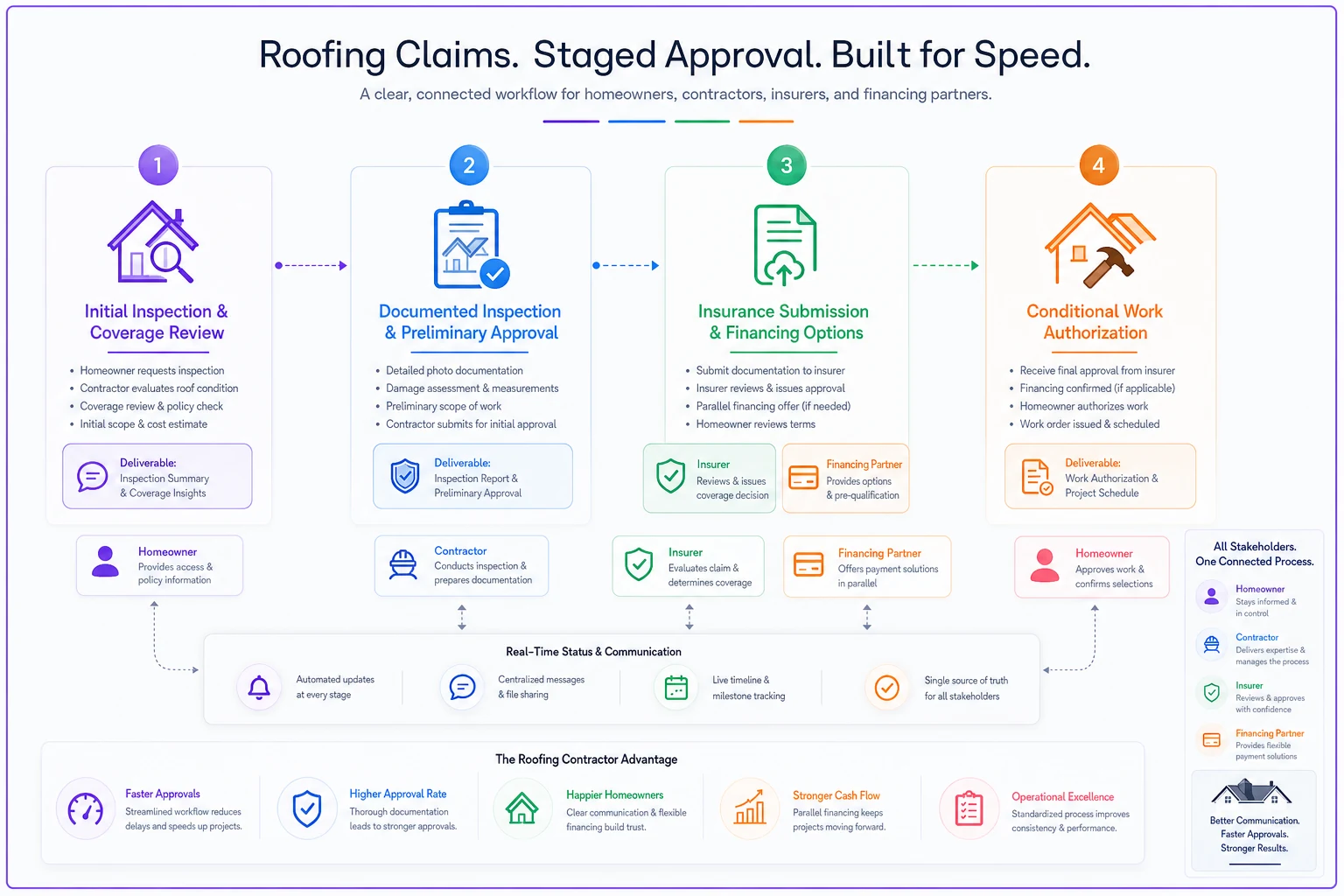

The old model was simple: find damage, document it, start work while insurance processes the claim. That model assumed insurance would eventually pay.

Stage 1: Initial inspection and homeowner coverage review Before anyone climbs a ladder, you pull the homeowner's actual policy documents. Not just the declaration page — the full policy with exclusions and limits. Run the numbers on their deductible versus the probable scope. If they have FAIR Plan coverage, you need to know exactly what their roof damage limit is. This conversation happens before you invest time in detailed inspection. Roughly 30% of initial contacts won't move forward once they understand their out-of-pocket responsibility.

Stage 2: Documented inspection with preliminary approval Your inspection now serves two masters — the homeowner and their insurance. Every photo, every measurement, every note needs to stand up to adjuster scrutiny while also giving the homeowner a clear picture of necessary work. The preliminary approval isn't about starting work. It's about getting the homeowner's written acknowledgment of the scope and their financial responsibility if insurance falls short. This document becomes critical when claims get partially denied or delayed.

Stage 3: Insurance submission with parallel financing options Submit to insurance, but don't wait for approval to explore financing. Most California homeowners facing $10,000+ deductibles need payment options. The contractors surviving this market have financing partnerships ready to deploy the moment insurance coverage gaps appear.

Stage 4: Conditional work authorization Work starts only with clear payment guarantees. Either insurance pre-approval, a homeowner deposit covering materials plus margin, or approved financing covering the full scope. No exceptions.

Require written homeowner acknowledgment of scope and financial responsibility before any work begins to avoid paying out of pocket later.

This might seem overly cautious, but contractors working without these gates are hemorrhaging money on jobs where insurance pays 60% of scope and homeowners can't cover the difference.

The adjuster coordination problem

Insurance companies are overwhelmed. California's FAIR Plan now covers nearly 5% of single-family homes, up from basically nothing a few years ago. Regular carriers are scrutinizing every claim to limit exposure. The result: adjusters are buried, and your claims sit in massive queues.

Smart contractors aren't waiting for adjusters anymore. They're actively managing the adjuster relationship from day one.

This starts with speaking their language. Your documentation needs to match their review checklist exactly. Include their preferred measurement methods. Reference their coverage guidelines in your scope notes. Make it impossible for them to kick your claim back for missing information.

But documentation alone won't accelerate approval. You need systematic follow-up that doesn't annoy adjusters but keeps your claim moving.

Set calendar reminders for every 72 hours after submission.

-

First contact confirms receipt.

-

Second asks about review timeline.

-

Third offers additional documentation.

-

Fourth escalates to a supervisor if there's still no response.

Keep a simple tracking spreadsheet with adjuster names, direct phone numbers, email addresses, response times, and approval patterns. You'll quickly figure out which adjusters move fast and which ones sit on claims. Route your urgent jobs accordingly when you have options.

The contractors getting claims approved in 10-15 days versus 45-60 days aren't lucky. They're running systematic processes that most crews don't even think about.

Customer communication scripts that prevent payment disasters

Your crew needs exact language for coverage conversations. Vague explanations create massive problems when homeowners realize their out-of-pocket costs are higher than expected.

Initial Coverage Verification Script: "Before we proceed with detailed inspection, let's review your coverage specifics. Can you pull up your insurance policy — not just the summary, but the actual coverage sections? We need to verify three numbers: your deductible amount, your roof damage coverage limit if you have FAIR Plan, and any exclusions that might apply."

Post-Inspection Reality Check: "Based on our inspection, the full replacement cost is approximately $24,000. With your $8,000 deductible, you'd need $8,000 upfront even if insurance approves everything. If they classify some damage as wear-and-tear, your portion could reach $12,000-14,000. Are you prepared for that potential cost?"

Financing Bridge Script: "Many homeowners in similar situations use our financing partners to cover the deductible and any coverage gaps. This lets you proceed with necessary repairs while insurance processes the claim. Would you like me to run some payment scenarios?"

Work Authorization Script: "We can begin work once we have either: full insurance approval, a deposit covering materials plus 30%, or approved financing for the total project cost. Which option works best for your situation?"

These scripts prevent the scenario where you complete work and then discover the homeowner can't pay their portion. Clear, documented communication protects both parties.

Building financial buffers for slow-pay scenarios

Cash flow management in restricted insurance markets requires different strategies than standard operations. You can't float jobs for 60-90 days when half your claims face coverage disputes.

The buffer strategy starts with deposit structures. Materials plus 30% minimum for any job where insurance coverage is uncertain. This isn't negotiable. Explain it as protecting both parties — you can't risk your operation on unpaid work, and they need a contractor who'll still be in business to honor warranties.

Progress payment schedules become essential for larger jobs.

| Phase | Payment |

|---|---|

| Tear-off and deck repair | 25% |

| Underlayment and ice barrier | 25% |

| Shingle installation | 25% |

| Final inspection and cleanup | Final 25% |

This keeps cash flowing even when insurance drags.

Consider separate pricing for insurance-dependent versus cash or financing jobs. Insurance jobs carry inherent payment delay risk. Price accordingly. A 10-15% premium for insurance-dependent work isn't unreasonable when payment might take 90 days.

Maintain a credit line specifically for insurance gap coverage. When you know insurance will eventually pay but need to keep crews working, a business credit line bridges the gap. The contractors struggling right now often lack this financial buffer.

Factor receivables when necessary. If you're sitting on $200,000 in approved but unpaid insurance claims, factoring companies will advance 80-85% immediately. Yes, you lose some margin, but it keeps operations running.

Technology infrastructure for claims management

The paperwork complexity of restricted insurance markets demands better systems than most contractors run. Email threads and spreadsheets can't handle the documentation, follow-up, and coordination requirements without things falling through the cracks.

Contractors managing this well have built out tech stacks specifically for claims management. Not fancy software for its own sake — just systematic information handling that prevents profitable jobs from becoming losses.

Photo documentation apps that timestamp and GPS-tag every image. When adjusters question damage timing, you have proof. These apps also enforce documentation standards by requiring specific shot types and quantities before an inspection can be marked complete.

Claim tracking platforms that centralize all communication with insurance companies. Every email, every call note, every document submission in one place. When claims stall, you have complete history for escalation.

Customer portal systems where homeowners can review documentation, approve scopes, and track claim status. This transparency cuts down on the "I didn't know it would cost that much" conversations that kill jobs mid-project.

AI-powered operational software is increasingly handling the coordination overhead that buries office staff — automatic adjuster follow-ups, document preparation matched to specific insurance company requirements, payment reconciliation that catches partial payments or missing supplementals. When every job requires significantly more documentation and coordination than it used to, automating the repetitive parts isn't a luxury, it's how you stay competitive.

This connects directly to the invoice and claims handoffs that determine whether you get paid promptly. When your claims documentation flows seamlessly into your invoicing process, payment delays drop significantly.

Adjusting sales and operations for the new reality

The restricted insurance market requires real shifts in how roofing companies operate. You're not just installing roofs anymore — you're running a financial services operation that happens to involve roofing.

Sales processes need a complete overhaul. The old "we'll handle your insurance claim" pitch doesn't work when insurance won't cover the full job. Sales reps need training on coverage types, deductible calculations, financing options, and realistic timeline expectations. They're essentially becoming insurance advisors who also sell roofs.

Operational capacity planning changes too. When a significant portion of approved jobs stall on financing or coverage gaps, you can't schedule crews assuming smooth workflow. Build 25-30% capacity buffer into your scheduling. Yes, this means occasional idle time, but it beats having crews sit for days when jobs fall through at the last minute.

Vendor relationships need renegotiation. Material suppliers need to understand your payment cycles are extending because of insurance delays. Negotiate longer terms or volume discounts that offset carrying costs. Some contractors are partnering with suppliers on financing programs that help homeowners handle coverage gaps.

Pricing models should reflect actual risk. Jobs with clear insurance pre-approval get standard pricing. FAIR Plan jobs with coverage caps need 15-20% premiums. High-deductible situations where homeowners need financing require different margin structures to offset payment risk.

The competitive advantage in restricted markets

Most contractors miss this: restricted insurance markets create opportunity for operationally disciplined companies. While competitors struggle with claims and cash flow, well-run operations can capture market share.

The winners share common characteristics. They document obsessively from first contact. They qualify homeowners' ability to pay before investing time. They maintain financial buffers for payment delays. They run systematic adjuster follow-up. They offer multiple financing options. They price appropriately for risk.

The real separator is operational infrastructure. Companies with proper claims management systems, automated documentation workflows, and integrated financial tracking can handle significantly more jobs than those running everything manually. When every job requires intensive coordination, operational efficiency becomes the competitive moat.

This isn't temporary. California's insurance situation will likely worsen before improving. Other states are watching similar patterns emerge. The contractors building proper operational infrastructure now will be in a much stronger position when restricted coverage becomes the norm elsewhere.

Moving forward in the new normal

The insurance squeeze isn't ending soon. Stanford's data shows the crisis expanding beyond fire zones into mainstream markets. This is the operating environment now, not a temporary disruption.

Start with honest assessment of your current operations. How many jobs in the last 90 days faced coverage issues? What percentage of receivables are past 60 days? How much crew time gets wasted on stalled approvals? The numbers usually surprise contractors who haven't been tracking carefully.

Build the financial buffers first. You need cash reserves or credit access to survive 90-day payment cycles. Without financial cushion, one bad month of coverage denials can sink an otherwise healthy operation.

Upgrade documentation and claims processes immediately. Every day you operate with weak documentation standards costs real money. Invest in proper tools and training. The upfront cost pays back quickly through better approval rates.

Train your entire team on the new reality. From sales reps to crew chiefs, everyone needs to understand coverage limitations and documentation requirements. One weak link in the communication chain creates payment disasters.

Most importantly, price for the market you're actually in, not the one you wish existed. Restricted insurance coverage adds operational complexity and financial risk. Your pricing needs to reflect that.

The roofing contractors succeeding in California's insurance squeeze aren't lucky. They've rebuilt their operations around documentation discipline, rigorous approval processes, and financial buffers. They've accepted that running a roofing company now means running a complex financial operation where installation is just one piece of the puzzle.

The sooner you align operations with this reality, the better positioned you'll be as insurance restrictions spread into other markets. This isn't a crisis to weather — it's a market shift that rewards operational discipline and punishes sloppy process.

The roofing contractors succeeding in California's insurance squeeze aren't lucky. They've rebuilt their operations around documentation discipline, rigorous approval processes, and financial buffers. They've accepted that running a roofing company now means running a complex financial operation where installation is just one piece of the puzzle.

The sooner you align operations with this reality, the better positioned you'll be as insurance restrictions spread into other markets. This isn't a crisis to weather — it's a market shift that rewards operational discipline and punishes sloppy process.

Ready to elevate your roofing operations?

Join hundreds of roofing contractors using Roofyly to streamline workflows, improve crew coordination, and enhance client satisfaction.